Health insurance claim help is something I desperately needed last spring when I ended up in the ER for what turned out to be a stupid kidney stone—seriously, who knew passing a rock could cost five grand?

I’m sitting here in my messy living room in suburban Chicago right now, December 30, 2025, snow piling up outside my window, coffee gone cold beside me, and I’m finally laughing about it because I figured this crap out the hard way. Like, health insurance claim help wasn’t some polished guide I found; it was me crying on hold with customer service for hours, messing up forms twice, and almost paying out of pocket before I got smart.

Anyway, if you’re dealing with this nightmare, here’s my real-talk health insurance claim help from someone who’s been there.

My Biggest Screw-Ups with Health Insurance Claim Help (And How I Fixed Them)

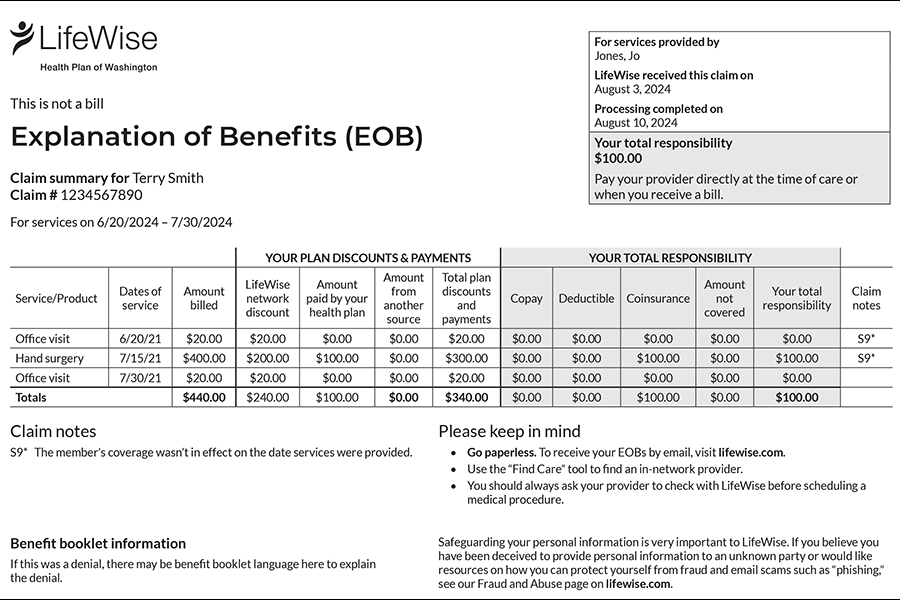

First off, I ignored the Explanation of Benefits (EOB) that came in the mail. Thought it was just junk. Big mistake. That thing isn’t a bill—it’s basically the insurance company’s diary entry on what they think they owe.

I threw the first one away, then panicked when the actual bill showed up for the full amount. Health insurance claim help tip #1: Read your damn EOB the second it arrives.

Mine said “not medically necessary” for some scan—uh, excuse me, kidney stones are necessary pain, thanks. I learned to highlight codes, Google them (like CPT codes are your friend), and call the provider to match up what they billed vs. what insurance saw.

The Denied Claim Drama – Real Health Insurance Claim Help That Worked for Me

So yeah, denied. I freaked. Called the insurance hotline and got transferred four times, ended up yelling at a poor rep who probably hates their job more than I hated my stone.

Then I calmed down, found their appeals page online, and realized you have 180 days usually to fight back. My health insurance claim help breakthrough? Writing a polite but firm appeal letter with doctor notes attached.

Pro tip: Get your doctor to write a letter of medical necessity. Mine did it for free after I begged. According to Healthcare.gov, appeals work about 50% of the time if you do it right.

Here’s the basic steps I followed:

- Gather everything: EOB, bills, doctor notes, procedure reports.

- Call the insurance to ask exactly why denied (get reference number!).

- Submit appeal online or mail—track it like your life depends on it.

- Follow up every two weeks. Politely. Ish.

For official guidance, check out the U.S. Department of Health and Human Services appeals process here: https://www.hhs.gov/healthcare/about-the-aca/appeals/index.html

Surprise Bills and No Surprises Act – The Health Insurance Claim Help Hero We Needed

Half my bill was from an out-of-network anesthesiologist who swooped in without warning. Classic surprise bill. But luckily, the No Surprises Act kicked in (thanks, 2022 laws).

I didn’t even know about it until a friend mentioned it. Health insurance claim help gold: If it’s an emergency or you’re at an in-network hospital, they can’t balance bill you crazy amounts anymore.

I disputed it directly with the provider, referenced the law, and poof—adjusted to in-network rates. More info on that from CMS: https://www.cms.gov/nosurprises

A Medical Insurance Claim Form With A Red Approved Stamp Stock …

Organizing Your Mess – Practical Health Insurance Claim Help for Sanity

Now I have a folder system. Embarrassing it took a $5k scare, but whatever.

- One folder for EOBs

- One for paid bills

- One for disputes in progress

- Scan everything to my phone app (I use Adobe Scan, free)

And set calendar reminders for appeal deadlines. Seriously.

Wrapping This Up – You Got This

Look, health insurance claim help isn’t rocket science, but it feels like it when you’re stressed and in pain. I still get anxious opening medical envelopes, but now I know I can fight and usually win.

If you’re in the thick of it right now, start with reading that EOB and calling your insurance—ask for a “case manager” if it’s complicated. You’ve got rights, and most denials are fixable.

Drop your own horror stories in the comments if you want; misery loves company. Or better yet, share what worked for you. Stay warm out there (or cool, depending on your hemisphere), and here’s to getting those bills covered without losing your mind.

{kind=link}